Dear readers, below is a piece that went out to members and friends of Prometheus Macro Research on the 12th of February. We hope you find it informative. Note that although the trade’s horizon is multi-year, we take into account some shorter-term considerations such as positioning and sentiment, for the purposes of developing a compelling argument for action, as well as to attempt to gain an additional edge from timing.

Universally, markets tend to ascribe a greater risk premium to political uncertainty than they will to its antithesis. So, perhaps there is a subtle irony that I would develop a compelling argument for action on the long side, coincident to the announcement that the British Parliament has authorised Prime Minister May to begin the process of invoking Article 50 of the Lisbon Treaty. A consequence of the vote to leave the European Union succeeding in the referendum on the 23rd of June 2016. A vote which left the freshly minted portmanteau ‘Brexit’, indelibly imprinted upon the popular lexicon.

BEHAVIOURAL CONTEXT

I’ve written before about the implications of ideology in speculative and investment decision making in Biases in Trading, where I made the case that through an evolutionary tendency toward emotional reasoning and various other fallacies and biases, people are predisposed to mistakes when making trading decisions according to their underlying political ideology. Indeed, perhaps this is why I didn’t fully exploit the fall in the Sterling whilst I was confident the ‘leave’ vote would prevail. A lesson which reminds me to focus on expected value and the potential asymmetries of political outcomes.

Politically, I leant toward Brexit, yet I didn’t appreciate that the outcome of its triumph would be so significant in the Pound over the short-term. Nevertheless, with new information and the iconoclastic tendency to question ideas that to others might be sacrosanct; I am inclined to face the other way. As the politics of Britain leaving the European Union has unravelled, it has appeared to me the emotional fervour has been distinctly in the Remain camp. Thus, I contend it is rational to diverge from the crowd amidst this cynical frenzy, and instead embrace an opportunity.

FUNDAMENTAL CONTEXT

Let us consider, that to the many people around the world living in countries with a less well-entrenched rule of law – if at all – that presently the Pound represents an opportunity to buy a share in the common-law system at a steep discount. The assurance of the common law system, as well as the land rights and other liberties which come with it, is a significant factor in the robustness of the world’s most successful commercial economies. Similarly, as opposed to its counterparts in customary and religious law, common law underpins the geopolitical position of the countries who employ it, by attracting capital.

IMAGE 1: LEGAL SYSTEMS OF THE WORLD

Source: https://en.wikipedia.org/wiki/Common_law

It is no surprise then, that the 16% drop in the ‘cable’ since ‘Brexit’, puts the currency in value territory against the dollar on a Purchasing Power Parity (PPP) basis; as evidenced in the chart below provided by one of our members at The Macro Trader.

CHART 1: GBPUSD PPP Valuation with 20% Bands

HYPOTHESIS & TIME HORIZON

Given our behavioural, statistical and technical reasoning, then temporally speaking the British Pound is likely to be near a multi-year cyclical bottom.

TECHNICALS

The British Pound trade-weighted index is approximately in the 3rd percentile of observations over the past 17 years as evidenced below.

CHART 2: STERLING TRADE-WEIGHTED INDEX (TWI BPSP Index)

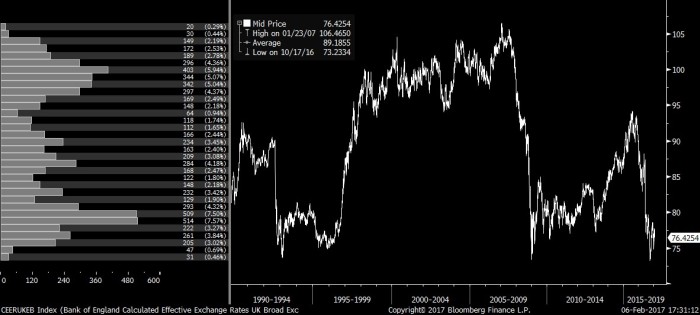

Whilst, the BOE Calculated Effective Exchange Rates UK Broad Index is presently in approximately the 4th percentile of observations since 1990.

CHART 3: STERLING TRADE-WEIGHTED INDEX (CEERUKEB Index)

Given these compelling statistical inferences, one must then consider the relative fundamental and technical characteristics of the Pound against various currencies.

GBPUSD

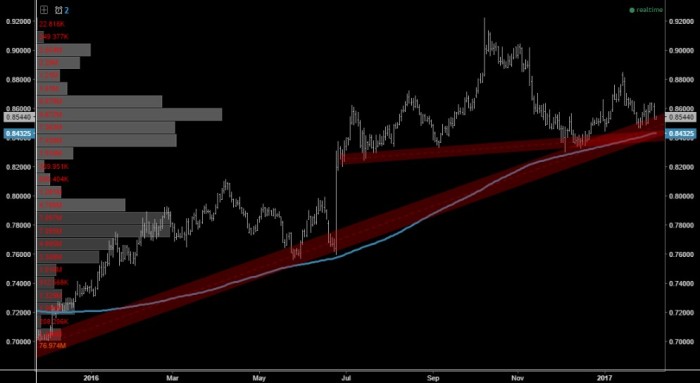

Technically speaking, the pound looks attractive on numerous fronts. The classicists are focusing on what many regard as a potential “double-bottom” pattern, indicated in red below, although a channel may be the more likely interpretation.

CHART 4: GBPUSD Daily with 200MA in Blue

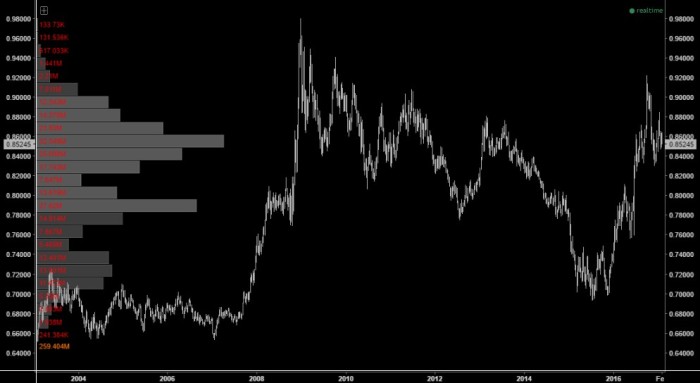

Further, on the weekly chart the cable is resting and potentially bouncing-off long-term trend support. From an elementary statistical standpoint, it is not unreasonable to anticipate a move toward the mean of the histogram on the left axis, which is why statistical extremes with support, such as these, are appealing. Particularly, considering it is currently within the 2nd percentile of observations since 1993.

CHART 5: GBP Weekly

Of course, currencies are priced relatively, thus other crosses need to be considered beyond simply the technical attractiveness vis-a-vis the dollar.

EURGBP

Similarly, on a daily basis, the euro-sterling appears to be a more compelling short, with a confluence of technical events occurring. Firstly, a seven-month head and shoulders pattern has the classical traders talking about a move which they measure down to the 74 handle. Further, the neckline of this chart happens to converge with both the 200-day moving average and an uptrend line that has held on the pair since it bottomed in late 2015.

CHART 6: EURGBP Daily with 200MA in Blue

Turning to the weekly, the cross doesn’t yield too much in terms of a constructive technical insight. Although, fundamentally speaking the euro seems like an ideal candidate to express this trade as the political uncertainty baton has now been passed from the United Kingdom to the European Union, whose fragility is far greater without the Brits as a member state. Indeed, this is heightened by the risks posed by the various European elections this year.

CHART 7: EURGBP Weekly

GBPJPY

The short term chart appears to have potentially bottomed and reversed trend, given the price looks to have almost cleared the 200 day moving average. Albeit, there is little else technically compelling about the cross in the short-term charts.

CHART 8: GBPJPY Daily with 200MA in Blue

However, one constructive observation is the long term support against the Yen which has held since the mid-nineties. Perhaps one’s view of whether Abenomics will devalue the Yen would be the dominant factor in deciding the Sterling-Yen cross is the best expression.

CHART 9: GBPJPY Weekly

Indeed, further consideration must be given to the regime of a given market and whether it fits with one’s strategy. In the case of sterling-yen, it is traditionally a great cross to trend follow as evidenced overleaf.

Our weekly trend-following model recently signalled a buy on the cross. As mentioned, historically this strategy works favourably, going back to the beginning of our data in mid-1975. Certainly, it is a somewhat cherry-picked, lowbrow observation and whilst it is important to avoid over-fitting to the past, one must also consider the particular characteristics of a given market.

CHART 10: GBPJPY Weekly Trend Following Model

Whilst we don’t follow this systematically, it does provide meaningful insight into the probabilities of the approach one might take on the sterling-yen cross.

CHART 11: GBPJPY Weekly Trend Following Model Performance Summary

POSITIONING & SENTIMENT

Positioning data for spot foreign exchange transactions is not available (hopefully one day), however we can look at the futures non-commercial positioning in the Sterling as a proxy. Notably, it is presently at relatively extreme levels vis-a-vis history. In fact, the levels are nearing the extremes set in 2013 when speculators and hedge funds were almost unanimously bearish, and wrong.

CHART 12: GBPUSD Weekly & COT Net Non-Commercials Speculative Positioning

As a behaviourist, one must consider that positioning is a real-time referenda on financial speculators’ sentiment, which evidenced by short positioning reaching the same extreme levels as 2013, is extremely bearish. Hence, we are inclined to take the other side.

CHART 13: GBPUSD Weekly & COT Non-Commercial Shorts Positioning

One of our members brought to our attention that these numbers must be adjusted for Open Interest, which he has done and ranked by percentiles on his site freecotdata.com. Presently, hedge fund positioning is in the 17th percentile, having recently increased from the lowest decile.

CHART 14: GBPUSD & COT Positioning Adjusted for Open Interest

VOLATILITY SURFACE

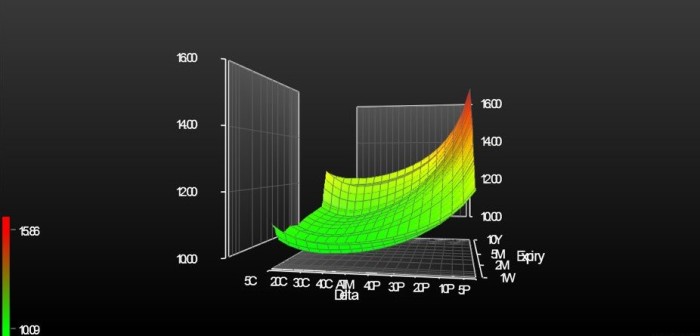

The GBPUSD volatility surface indicates market makers are more willing to write calls than puts presently. Rephrased and inverted, that means there is more demand to hedge via puts than calls. Suggesting that the market’s intersubjective probability assessment – or collective agreement of the Sterling’s future pricing – is fairly bearish. Consistent with our inferences from positioning data regarding the market’s sentiment.

CHART 15: GBPUSD Volatility Surface

Further, this skew indicates selling downside structures to the hedgers may be of interest, so we shall turn our attention to implied volatility overleaf.

IMPLIED VOLATILITY

GBPUSD one month implied volatility is presently quoted in approximately the 89th percentile of the last 5 years’ data, as evidenced by the chart below.

CHART 16: GBPUSD Implied Volatility

These implied volatility levels are invariably elevated as a function of the grey swan-like impact of Brexit. Arguably, they price a measure of recency bias given the likelihood of another ~14 sigma daily move is low, which fits with my unpretentious observation that markets ascribe a greater risk premium to political uncertainty than to its antithesis.

This view justifies the perspective that both implied volatility and realised volatility will revert toward the mean as markets re-calibrate to a more certain political reality, in a market where the weak hands have been shaken out due to such high realised volatility.

Simply put, less fragile positions reduce the probability of high realised volatility. However, this is not to suggest exposure to unlimited loss structures is ever prudent. Instead, loss-limited structures, such as short put spreads; enable the ability to collect this elevated risk premium with a pre-defined and limited loss. Similarly, for those who trade esoteric structures, selling one-touch puts provides a similar return profile to put spreads as they are loss-limited, non-recourse structures.

EXPRESSION & STRATEGY

Long: GBPUSD & GBPJPY (trend following)

Short: EURGBP

Derivatives: short gamma GBPUSD can add carry to the position

Rates: cheapen VaR by receiving LZ17

Equities: we shall follow up with our equity views when the timing is right

Given we have a multi-year time horizon on the Sterling and a fundamentally bearish bias over a similar temporal horizon on the euro, a strategic long with no stop is our chosen methodology. With the sterling-yen, trend following is our chosen strategy given its historical efficacy.

Further, whilst we don’t take unlimited-loss short gamma positions, selling the downside on GBPUSD remains an attractive proposition, particularly taking into consideration the skew and richness of the implied volatility, as well as providing the opportunity to add carry to the position.

PROBABILITIES & POSITION SIZING

Typically our position sizing process is one shamelessly adopted from James Leitner of Falcon Management Corporation who was kind enough to share his Kelly Criterion or optimal leverage sizing process with some of the Drobny Global Advisors members along with the presentation The Evolution of a Macro Portfolio. However, given we haven’t yet expanded upon this methodology and our variant of its application – looking at frequentist and intersubjective probabilities, and the expectations gap between them – for the purposes of keeping this piece as concise as possible we will leave this to a later date. Further, given a 100% allocation to a single currency exposure is everyone’s default position, sizing strategic long-term currency positions requires a somewhat different process to the one we would otherwise undertake for other asset classes. Of the various approaches one might employ, a risk-targeted approach is what we shall adopt. Accordingly, it is necessary for those who implement this trade to size according to their own risk tolerance. We shall follow up with an explanation of our sizing methodology and an introduction to our macro tracking portfolio in the coming days.

Best,

Carl Hodson-Thomas

Nb. For those of you interested in learning more about receiving our research, please visit http://www.prometheus-am.com.au/subscribe/

{kind=link}

{kind=link}